Systematic Investment Plans (SIPs) have gained immense popularity as a convenient and disciplined way to invest in mutual funds. However, one common question that often arises among investors is, “Can I withdraw SIP anytime?” In this comprehensive guide, we will explore the liquidity aspect of SIPs, explaining when and how you can withdraw your investments while maintaining the financial discipline that SIPs offer.

Before diving into the liquidity aspect of SIPs, let’s briefly understand what SIPs are and how they work.

SIPs are a method of investing in mutual funds that allow investors to contribute a fixed amount of money at regular intervals, typically monthly. These investments accumulate over time and are used to purchase units of a mutual fund, thus spreading the investment over various market conditions. SIPs are known for their simplicity, affordability, and potential to offer attractive returns over the long term.

The answer to this question is both yes and no, depending on the context. Let’s explore the scenarios in which you can withdraw your SIP investments.

Yes, you can make partial withdrawals from your SIP investments at any time, subject to certain conditions set by the mutual fund house. However, it’s important to understand that making partial withdrawals may affect the long-term growth potential of your investment.

Yes, you can fully withdraw your SIP investments after the predetermined SIP tenure is completed, which is typically a minimum of three years.

Yes, you can stop future SIP installments at any time without any penalty. If you choose to do so, your existing SIP investments will continue to grow based on market conditions.

In cases of financial emergencies, some mutual funds offer the option to withdraw your investments, even before the completion of the SIP tenure. However, this may be subject to specific terms and conditions, and the mutual fund may charge applicable exit loads or penalties.

In summary, while SIPs provide the flexibility to make partial withdrawals during the SIP tenure, the complete withdrawal of your investments is typically allowed after the predetermined SIP tenure is completed. Stopping future SIP installments is also hassle-free and can be done at any time. It’s important to consider your financial goals, investment horizon, and liquidity needs when deciding on partial or full withdrawals from your SIPs.

SIPs are designed to encourage disciplined, long-term investing, and withdrawing funds prematurely may impact your ability to maximize returns. Before making any withdrawal decisions, it’s advisable to consult with a financial advisor who can provide personalized guidance based on your unique financial situation and objectives.

This post was last modified on May 9, 2024 3:27 am

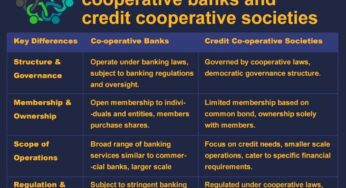

Co-operative Banks vs. Credit Co-operative Societies In the world of banking and finance, institutions like co-operative banks and credit co-operative…

The Securities and Exchange Board of India (SEBI) regulates the investment advisory sector in India through the SEBI (Investment Advisers)…

Following the introduction of AePS in India, mPOS devices began to proliferate across the country. These palm-sized handheld mPOS devices…

If you're looking for a dependable and affordable mobile point-of-sale (mPOS) solution, the PAX D180 is an excellent choice. This…

Paynearby and Spice Money stand out as two prominent companies offering similar services but with subtle distinctions. Let's delve into…

As a seasoned AEPS (Aadhaar Enabled Payment System) service distributor with 6 years of experience, I can attest to the…