Fixed deposits (FDs) are popular investment options that offer stability and assured returns. The Post Office, with its extensive reach and trusted reputation, provides individuals with an accessible avenue for investing in FDs. If you’re considering opening an FD with the Post Office, one common question you may have is: How many years will it take for your investment to double? In this article, we will delve into the factors that determine the doubling period of FDs in Post Office, allowing you to make informed decisions about your investment.

Post Office Fixed Deposits are a type of time deposit offered by India Post. They provide individuals with a safe investment option backed by the government. Post Office FDs have a fixed tenure and interest rate, making them a popular choice for risk-averse investors.

Several factors influence the doubling period of FDs in Post Office:

To estimate the doubling period of an FD in Post Office, we can apply the Rule of 72, a simple formula used to approximate the time it takes for an investment to double. The formula is as follows:

Doubling Time = 72 / Interest Rate

For instance, if the interest rate offered by the Post Office is 7%, the doubling period would be:

Doubling Time = 72 / 7 = 10.29 years

Therefore, it would take approximately 10.29 years for your investment to double with a 7% interest rate.

It’s important to note that the Rule of 72 provides an approximate estimate and may not account for factors like compounding frequency and fluctuations in interest rates. However, it can serve as a useful starting point for understanding the doubling period of your investment.

While estimating the doubling period is crucial, there are other factors to consider when investing in Post Office FDs:

Post Office Fixed Deposits offer a reliable and accessible investment option for individuals seeking stability and assured returns. While the exact doubling period of an FD in Post Office depends on factors such as the interest rate, compounding frequency, and tenure, the Rule of 72 can provide a rough estimation. It’s important to consider other factors like tax benefits, premature withdrawal policies, and the safety offered by the Post Office.

Investing in Post Office FDs requires careful evaluation of your financial goals, risk appetite, and liquidity needs. By understanding the doubling period and the associated considerations, you can make well-informed decisions that align with your investment objectives. Remember to conduct thorough research, compare interest rates, and seek professional advice if required. Post Office FDs can serve as a valuable component of your investment portfolio, supporting your financial aspirations and providing stability in uncertain times.

This post was last modified on July 3, 2023 12:05 pm

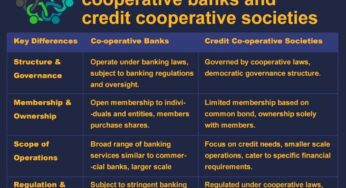

Co-operative Banks vs. Credit Co-operative Societies In the world of banking and finance, institutions like co-operative banks and credit co-operative…

The Securities and Exchange Board of India (SEBI) regulates the investment advisory sector in India through the SEBI (Investment Advisers)…

Following the introduction of AePS in India, mPOS devices began to proliferate across the country. These palm-sized handheld mPOS devices…

If you're looking for a dependable and affordable mobile point-of-sale (mPOS) solution, the PAX D180 is an excellent choice. This…

Paynearby and Spice Money stand out as two prominent companies offering similar services but with subtle distinctions. Let's delve into…

As a seasoned AEPS (Aadhaar Enabled Payment System) service distributor with 6 years of experience, I can attest to the…