Income tax is an integral part of a nation’s revenue generation system, and understanding its nuances is crucial for every taxpayer. One important aspect of income tax assessment is Section 143(1), which plays a significant role in ensuring accurate and timely tax filing. In this guide, we will explore the intricacies of Income Tax Section 143(1), its purpose, implications, and how it affects taxpayers in India.

Income Tax Section 143(1) falls under the Income Tax Act of India and pertains to the preliminary assessment of tax returns submitted by taxpayers. The section essentially deals with processing the return of income and determining the tax liability of the taxpayer based on the information provided in the return.

The primary purpose of Section 143(1) is to carry out a preliminary assessment of the return filed by the taxpayer. Once the taxpayer submits their income tax return, the income tax department reviews the details provided and performs a preliminary assessment to validate the correctness of the information. This includes verifying the mathematical accuracy of calculations, ensuring that all income sources are correctly reported, and cross-checking deductions and exemptions claimed.

Upon processing the return under Section 143(1), the income tax department may take one of the following actions:

In case the income tax department identifies discrepancies or adjustments in the return, the taxpayer has the option to respond to the intimation. If the taxpayer agrees with the adjustments, they can pay the additional tax amount (if applicable) within the specified timeline mentioned in the intimation. On the other hand, if the taxpayer disagrees with the adjustments, they can file a rectification request online and provide necessary explanations or evidence to support their claim.

Income Tax Section 143(1) underscores the importance of accurate and thorough reporting of financial details in the tax return. Incorrect reporting can lead to discrepancies, which may result in additional tax liabilities, penalties, or even legal consequences. It is advisable for taxpayers to maintain proper documentation, accurately report all sources of income, and keep track of deductions claimed.

In summary, Income Tax Section 143(1) serves as a critical step in the income tax assessment process in India. It ensures that taxpayers’ returns are reviewed for accuracy and completeness, promoting transparency and compliance. Taxpayers should be vigilant when filing their returns, review any intimations received under this section, and respond promptly if adjustments are required. By understanding and adhering to the provisions of Section 143(1), taxpayers can contribute to a smoother and more efficient income tax assessment process.

This post was last modified on August 29, 2023 5:10 am

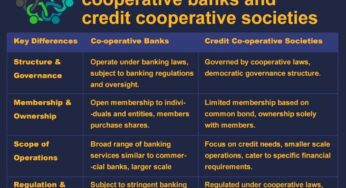

Co-operative Banks vs. Credit Co-operative Societies In the world of banking and finance, institutions like co-operative banks and credit co-operative…

The Securities and Exchange Board of India (SEBI) regulates the investment advisory sector in India through the SEBI (Investment Advisers)…

Following the introduction of AePS in India, mPOS devices began to proliferate across the country. These palm-sized handheld mPOS devices…

If you're looking for a dependable and affordable mobile point-of-sale (mPOS) solution, the PAX D180 is an excellent choice. This…

Paynearby and Spice Money stand out as two prominent companies offering similar services but with subtle distinctions. Let's delve into…

As a seasoned AEPS (Aadhaar Enabled Payment System) service distributor with 6 years of experience, I can attest to the…