The Marginal Cost of Funds Based Lending Rate, or MCLR, is a key interest rate used by banks in India to determine the minimum interest rate at which they can lend money to borrowers. In this blog article, we’ll take a closer look at what the MCLR is, how it is calculated, and what it means for borrowers in India.

The MCLR is the minimum interest rate that a bank can charge on loans. It was introduced by the Reserve Bank of India (RBI) in 2016 as a replacement for the base rate system. The MCLR system is based on the actual cost of funds for the bank and is meant to be more transparent and responsive to changes in market conditions.

The MCLR is calculated based on four components:

The MCLR is calculated by taking into account these four components and adding a spread or a margin. The spread is the bank’s profit margin and can vary from bank to bank.

The MCLR is an important factor that determines the interest rate that borrowers pay on their loans. Banks usually offer loans at an interest rate that is a certain percentage above the MCLR. For example, a bank may offer a home loan at MCLR plus 0.5%.

When the MCLR goes up or down, the interest rate on the loan also changes. This means that borrowers with loans linked to the MCLR will see their monthly payments go up or down depending on the changes in the MCLR.

Borrowers should also be aware that the MCLR may not be the same for all types of loans or all borrowers. Banks may charge different MCLR rates for different tenors or for loans of different amounts. Borrowers should also be aware of any additional charges or fees that may be associated with their loans.

The MCLR is an important interest rate that borrowers in India should be aware of. It is calculated based on the bank’s cost of funds and is used to determine the minimum interest rate that banks can charge on loans. Borrowers with loans linked to the MCLR should be aware that their interest rate and monthly payments may go up or down depending on changes in the MCLR.

A. The MCLR is a key interest rate that is used by banks in India to determine the minimum interest rate at which they can lend money to borrowers. It was introduced by the Reserve Bank of India (RBI) in 2016 as a replacement for the base rate system.

A. The MCLR is calculated based on four components: marginal cost of funds, operating costs, tenor premium, and marginal cost of maintaining cash reserve ratio (CRR). These components are added together, and a spread or margin is added to determine the final MCLR.

A. No, not all loans are linked to the MCLR. Some loans may be linked to other interest rates, such as the base rate or the repo rate.

A. The MCLR is reviewed and revised by banks on a monthly basis, depending on changes in their cost of funds.

A. No, borrowers cannot negotiate the MCLR with their bank. However, they may be able to negotiate the spread or margin that is added to the MCLR to determine their final interest rate.

A. Yes, the MCLR can go down if the bank’s cost of funds decreases. This would result in a decrease in the interest rate for borrowers.

A. Borrowers with loans linked to the MCLR will see their monthly loan repayments go up or down depending on changes in the MCLR. When the MCLR goes up, the interest rate on the loan will increase, resulting in higher monthly payments. When the MCLR goes down, the interest rate on the loan will decrease, resulting in lower monthly payments.

A. The MCLR system is meant to be more transparent and responsive to changes in market conditions. It allows borrowers to benefit from decreases in the bank’s cost of funds, and it provides more clarity on how the interest rate on a loan is calculated.

A. The MCLR system can be complex, with different MCLR rates for different tenors and types of loans. It may also be difficult for borrowers to compare MCLR rates between different banks. Additionally, the MCLR system may not always result in lower interest rates for borrowers, as banks may add a high spread or margin to the MCLR.

A. Yes, borrowers may be able to switch to a different interest rate if they are unhappy with the MCLR. However, there may be charges or fees associated with switching to a different interest rate, and the new interest rate may not always be lower than the MCLR.

This post was last modified on April 24, 2023 8:25 am

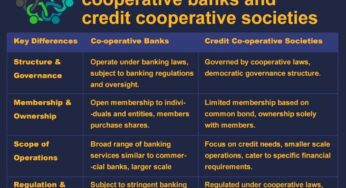

Co-operative Banks vs. Credit Co-operative Societies In the world of banking and finance, institutions like co-operative banks and credit co-operative…

The Securities and Exchange Board of India (SEBI) regulates the investment advisory sector in India through the SEBI (Investment Advisers)…

Following the introduction of AePS in India, mPOS devices began to proliferate across the country. These palm-sized handheld mPOS devices…

If you're looking for a dependable and affordable mobile point-of-sale (mPOS) solution, the PAX D180 is an excellent choice. This…

Paynearby and Spice Money stand out as two prominent companies offering similar services but with subtle distinctions. Let's delve into…

As a seasoned AEPS (Aadhaar Enabled Payment System) service distributor with 6 years of experience, I can attest to the…