Section 44ADA Example : Suppose Mr. Ravi is a freelance graphic designer and operates his business as a sole proprietor. In the financial year 2022-2023, his gross receipts from graphic design projects amounted to ₹40 lakhs. Let’s see how Section 44ADA applies to his taxation.

Under Section 44ADA, eligible professionals can declare their taxable income at a prescribed rate of 50% of their gross receipts. In this case, Mr. Ravi’s taxable income would be calculated as follows:

Gross Receipts: ₹40,00,000 Taxable Income (50% of Gross Receipts): ₹20,00,000

Therefore, Mr. Ravi’s taxable income for the financial year would be ₹20 lakhs.

Now, let’s compare this with the regular income tax computation under the Income Tax Act.

Suppose Mr. Ravi had maintained detailed books of accounts and after deducting business expenses, his net profit from the graphic design business amounted to ₹15 lakhs.

Under the regular income tax computation, Mr. Ravi would have to pay tax on the net profit of ₹15 lakhs. The tax liability would depend on the applicable tax slab rates, deductions, and exemptions as per the Income Tax Act.

However, by opting for Section 44ADA, Mr. Ravi can benefit from a simplified tax computation. In this case, his taxable income is deemed to be ₹20 lakhs, which is higher than the net profit of ₹15 lakhs calculated through regular accounting methods. Hence, Mr. Ravi’s tax liability would be calculated on the deemed income of ₹20 lakhs under Section 44ADA.

By choosing the presumptive taxation scheme under Section 44ADA, Mr. Ravi can enjoy the benefits of reduced compliance burden and potentially lower tax liability. However, it is important to note that once a taxpayer opts for Section 44ADA, they are required to continue with this scheme for subsequent years, subject to meeting the eligibility criteria.

It is advisable for Mr. Ravi to consult a tax professional or a chartered accountant to assess his specific tax situation, understand the implications of Section 44ADA, and determine the most advantageous approach for his business.

This example is for illustrative purposes only, and the tax liability may vary depending on various factors such as deductions, exemptions, and changes in tax laws. It is recommended to consult a tax professional for accurate and personalized tax advice.

This post was last modified on May 31, 2023 9:22 am

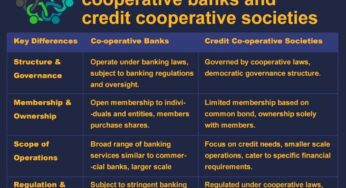

Co-operative Banks vs. Credit Co-operative Societies In the world of banking and finance, institutions like co-operative banks and credit co-operative…

The Securities and Exchange Board of India (SEBI) regulates the investment advisory sector in India through the SEBI (Investment Advisers)…

Following the introduction of AePS in India, mPOS devices began to proliferate across the country. These palm-sized handheld mPOS devices…

If you're looking for a dependable and affordable mobile point-of-sale (mPOS) solution, the PAX D180 is an excellent choice. This…

Paynearby and Spice Money stand out as two prominent companies offering similar services but with subtle distinctions. Let's delve into…

As a seasoned AEPS (Aadhaar Enabled Payment System) service distributor with 6 years of experience, I can attest to the…