Equity Linked Savings Schemes (ELSS) are a popular investment option in India, known for their potential to provide tax benefits along with the opportunity for wealth creation. However, ELSS investments come with a unique feature known as the “lock-in period.” In this comprehensive guide, we will delve into the concept of the ELSS lock-in period, its significance, and provide real-world examples to help you make informed investment decisions.

The lock-in period for ELSS funds is the duration during which investors are not allowed to redeem or withdraw their investments. This lock-in period is a distinctive feature of ELSS and serves a specific purpose – to encourage long-term investment in equities while providing tax benefits.

The ELSS lock-in period serves multiple purposes:

Amar, a salaried individual, is looking to reduce his taxable income. He decides to invest ₹1.5 lakh in an ELSS fund. By doing so, he not only enjoys a tax deduction but also has the opportunity to earn potential returns on his investment. However, he must be aware that his investment will be locked in for three years.

Pooja, a young professional with a long-term financial goal, chooses ELSS to invest her surplus income. She understands that the lock-in period aligns with her goal of wealth creation over the next decade. By staying invested beyond the lock-in period, she aims to benefit from the compounding effect of her investments.

Rahul is in need of a financial safety net and considers ELSS as an investment option. However, he must be cautious as ELSS investments are not liquid during the lock-in period. Rahul decides to allocate a portion of his emergency fund to investments that offer easier liquidity, such as a savings account or fixed deposits.

The ELSS lock-in period is a crucial aspect of these tax-saving mutual funds. While it restricts access to your invested capital for three years, it offers the dual advantage of tax benefits and the potential for wealth creation over the long term. Understanding the significance of the lock-in period and aligning it with your financial goals is essential for making informed investment decisions. Always consult with a financial advisor before making investment choices to ensure they align with your unique financial situation and objectives.

This post was last modified on October 4, 2023 12:52 pm

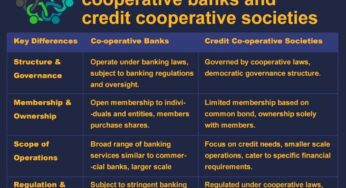

Co-operative Banks vs. Credit Co-operative Societies In the world of banking and finance, institutions like co-operative banks and credit co-operative…

The Securities and Exchange Board of India (SEBI) regulates the investment advisory sector in India through the SEBI (Investment Advisers)…

Following the introduction of AePS in India, mPOS devices began to proliferate across the country. These palm-sized handheld mPOS devices…

If you're looking for a dependable and affordable mobile point-of-sale (mPOS) solution, the PAX D180 is an excellent choice. This…

Paynearby and Spice Money stand out as two prominent companies offering similar services but with subtle distinctions. Let's delve into…

As a seasoned AEPS (Aadhaar Enabled Payment System) service distributor with 6 years of experience, I can attest to the…