The Daily Deposit Scheme is a unique banking initiative designed to cater specifically to daily wage earners, small traders, and individuals with irregular income streams. In India, Co-operative banks play a crucial role in promoting financial inclusion by offering this scheme. Let’s learn more in details about how it works, what are the benefits of it?

The primary goal of the Daily Deposit Scheme is to encourage regular savings among individuals who earn daily wages or have unpredictable income patterns. By allowing small deposits on a daily basis, this scheme aims to instill financial discipline and provide a safe path for collecting funds.

Unlike traditional fixed deposits, where you deposit a lump sum amount for a fixed tenure, the Daily Deposit Scheme allows you to contribute small sums daily. You can start with as little as Rs. 25 per day.

One of the unique feature of this scheme is doorstep collection. An authorized agent from the co-operative bank visits the account holder’s residence or workplace to collect the daily deposit. This convenience ensures that even those with busy schedules can get benefit of Daily Deposit Scheme.

The interest rate on daily deposits is typically modest, but it accumulates over time. However, there’s a catch: if you close the account before a specified period (usually eight or nine months), no interest is paid and there may be no penalty. In case of pre maturity closure, a 3% to 4% commission is deducted from the deposited amount and other taxes may be applicable.

Financial Inclusion: The scheme targets marginalized sections of society, providing them with access to formal banking services. It bridges the gap between daily wage earners and the banking system.

Flexible Deposits: Participants can adjust their daily deposit amounts based on their income fluctuations. This flexibility makes it suitable for irregular earners.

No Lump Sum Pressure: Unlike traditional fixed deposits, where a lump sum is required upfront, the Daily Deposit Scheme allows gradual savings without burdening the depositor.

Agent Employment: The scheme generates employment opportunities for agents who collect deposits from account holders. It’s a win-win situation for both the bank and the agents.

Long-Term Commitment: To maximize returns, consider keeping the account active for at least eight to nine months. Early withdrawals result in commission deductions.

Interest Rate: While the interest rate may be lower than other investment options, the cumulative effect over time can still be significant. Some co-operative banks provides interest up 6% (Reducing Interest rate)

Risk Profile: Daily deposits are safe, but they don’t offer high returns. Investors seeking higher yields should explore other investment opportunities.

The Daily Deposit Scheme in co-operative banks serves as a financial lifeline for those who rely on daily earnings. By fostering a savings habit and providing doorstep convenience, it contributes to financial stability and inclusion. As an investor, weigh the pros and cons carefully before participating in this scheme.

This post was last modified on April 9, 2024 6:01 am

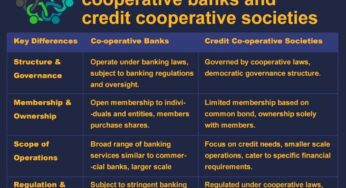

Co-operative Banks vs. Credit Co-operative Societies In the world of banking and finance, institutions like co-operative banks and credit co-operative…

The Securities and Exchange Board of India (SEBI) regulates the investment advisory sector in India through the SEBI (Investment Advisers)…

Following the introduction of AePS in India, mPOS devices began to proliferate across the country. These palm-sized handheld mPOS devices…

If you're looking for a dependable and affordable mobile point-of-sale (mPOS) solution, the PAX D180 is an excellent choice. This…

Paynearby and Spice Money stand out as two prominent companies offering similar services but with subtle distinctions. Let's delve into…

As a seasoned AEPS (Aadhaar Enabled Payment System) service distributor with 6 years of experience, I can attest to the…