In the realm of personal finance, Fixed Deposits (FDs) stand as a tried-and-true investment option that offers stability and assured returns. One of the core aspects that makes FDs appealing is the concept of interest, which allows individuals to earn passive income on their deposited funds over a predetermined period. In this article, we’ll delve into the mechanics of interest on fixed deposits, understanding how it is calculated, the factors that influence it, and why it matters to investors.

Interest on fixed deposits can be likened to the compensation you receive for allowing the bank to hold onto your money for a specific period. When you invest in an FD, you’re essentially lending money to the bank, which, in return, agrees to pay you interest on that amount.

The interest earned on FDs is the reward for locking your money away and not accessing it during the agreed tenure. It’s this reward that can make FDs an attractive investment choice for individuals looking for a secure and predictable way to grow their savings.

The calculation of interest on fixed deposits is typically based on the principal amount, the interest rate, and the tenure of the deposit. There are two main methods used to calculate interest on FDs:

Simple interest is calculated only on the initial principal amount. The formula for calculating simple interest is:Interest = Principal × Rate × TimeWhere:

Compound interest is calculated on both the initial principal amount and the accumulated interest from previous periods. It’s the more common method used by banks to calculate interest on fixed deposits. The formula for calculating compound interest is:A = P × (1 + r/n)^(nt)Where:

Interest is the cornerstone of fixed deposits, transforming them into a reliable investment option for a wide range of individuals. Whether you opt for simple or compound interest, the concept remains the same: you’re rewarded for allowing the bank to use your money for a fixed period. Understanding the mechanics of interest calculation, the factors that influence interest rates, and the importance of interest on fixed deposits empowers you to make informed investment decisions.

Before investing in fixed deposits, it’s advisable to compare interest rates across various banks, assess your financial goals, and consider the prevailing economic conditions. Fixed deposits can be a valuable tool in your financial arsenal, offering stability, predictability, and a steady source of income over time.

This post was last modified on August 9, 2023 10:44 pm

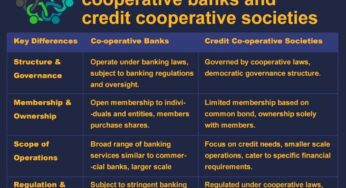

Co-operative Banks vs. Credit Co-operative Societies In the world of banking and finance, institutions like co-operative banks and credit co-operative…

The Securities and Exchange Board of India (SEBI) regulates the investment advisory sector in India through the SEBI (Investment Advisers)…

Following the introduction of AePS in India, mPOS devices began to proliferate across the country. These palm-sized handheld mPOS devices…

If you're looking for a dependable and affordable mobile point-of-sale (mPOS) solution, the PAX D180 is an excellent choice. This…

Paynearby and Spice Money stand out as two prominent companies offering similar services but with subtle distinctions. Let's delve into…

As a seasoned AEPS (Aadhaar Enabled Payment System) service distributor with 6 years of experience, I can attest to the…