Section 10(13A) of the Income Tax Act provides a significant tax exemption to individuals who receive House Rent Allowance (HRA) as part of their salary package. This section allows taxpayers to claim an exemption on a portion of their HRA, thereby reducing their taxable income. In this article, we will delve into the details of Section 10(13A) and explore how it benefits taxpayers.

Section 10(13A) is specifically related to the exemption of House Rent Allowance. It states that if an employee receives HRA as a part of their salary, they can claim a deduction on a certain portion of it. The objective is to provide relief to salaried individuals who incur rental expenses.

To claim the HRA exemption under Section 10(13A), taxpayers need to fulfill the following conditions:

The HRA exemption is calculated using the following parameters:

The least of the following three amounts is considered for HRA exemption:

Let’s consider an example to illustrate the calculation of HRA exemption:

Mr. Sharma, an employee in a metro city, receives a basic salary of Rs. 50,000 per month, with an HRA component of Rs. 20,000 per month. He pays a monthly rent of Rs. 18,000.

In this case, the least of the above three amounts is Rs. 13,000. Therefore, Rs. 13,000 will be considered as the HRA exemption for Mr. Sharma.

Section 10(13A) of the Income Tax Act provides a significant tax benefit to salaried employees who receive HRA as a part of their salary package. Understanding the conditions for claiming exemption and the calculation methodology can help taxpayers optimize their tax savings. It is essential to maintain proper documentation and receipts of rent paid to claim the exemption accurately. Consulting with a tax professional or referring to the relevant tax laws and guidelines can provide further clarity on HRA exemptions and compliance requirements

This post was last modified on May 6, 2023 9:04 am

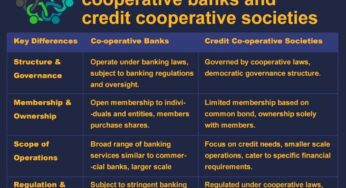

Co-operative Banks vs. Credit Co-operative Societies In the world of banking and finance, institutions like co-operative banks and credit co-operative…

The Securities and Exchange Board of India (SEBI) regulates the investment advisory sector in India through the SEBI (Investment Advisers)…

Following the introduction of AePS in India, mPOS devices began to proliferate across the country. These palm-sized handheld mPOS devices…

If you're looking for a dependable and affordable mobile point-of-sale (mPOS) solution, the PAX D180 is an excellent choice. This…

Paynearby and Spice Money stand out as two prominent companies offering similar services but with subtle distinctions. Let's delve into…

As a seasoned AEPS (Aadhaar Enabled Payment System) service distributor with 6 years of experience, I can attest to the…